- Home

- News

- Company news

- 中國(guó)互聯網保險發展簡史

之前的(de)文(wén)章(zhāng)提到(dà ∑§€o)了(le)互聯網+保險是(shì)大(dà)↓↑&勢所趨,那(nà)麽中國(guó)的(de)互聯網保險是(shì)如(rú)何從(cóng)萌芽"←發展,到(dào)現(xiàn)在的(de)欣欣向&→榮。今天就(jiù)來(lái)探討(tǎo)一(yī)下(xià)中國(β±&guó)互聯網的(de)發展簡史。

一(yī)般來(lái)說(shuō),中國(guó)互聯網保險行(xín✔$•g)業(yè)的(de)發展截止目前可(kě)分(fēn)為(w $èi):萌芽期,起步期,探索期,積累期,發展期,爆發期。

互聯網保險的(de)興起,歸根結底是(shì)消費(fèi)者日(↔¥rì)益增值的(de)投保需求與線下(xià)保險行(xíng)業(yè)不(bù)夠☆≤完善的(de)發展之間(jiān)的(de)沖突引發的(de)。國(gu♦<ó)內(nèi)消費(fèi)者的(de)保險意識,>Ω保險理(lǐ)念随著(zhe)經濟的(de)提升有(yǒλ♣πu)了(le)本質上(shàng)的(de)變化(huà)。從(cóngγσγ¥)之前的(de)聽(tīng)到(dào)保險就(jiù)怕,就(γ™γjiù)退,逐步轉化(huà)為(wèi)希望主動了(le)解保險,主動投保。↓←↔φ而由于線下(xià)理(lǐ)賠慢(màn),産品不(bù)夠豐富等 ✔≈原因,消費(fèi)者不(bù)再滿足線下(xià)的(de)保險産品與服務,于是(shì)乎互聯€↔$網保險應運而生(shēng)。

互聯網保險發展萌芽期:1997~2004 年(nián)。該階段,互聯網保↔≥&↑險以宣傳和(hé)科(kē)普為(wèi)主。

1997 年(nián)底,中國(guó)保險信息網誕生(shēng),是(shì)我♣¥∏國(guó)**面向保險市(shì)場(cε§ £hǎng)和(hé)保險公司內(nèi)部的(de)專業(yè)中文±•±(wén)網站(zhàn),也(yě)是(δ☆shì)我國(guó)保險行(xíng)業™≈'<(yè)*早的(de)第三方網站(zhàn);2000 年σ×(nián) 3 月(yuè),“ 網險網” **實© π現(xiàn)了(le)網上(shàng)投§♠§★保功能(néng);2001 年(nián) 3 月(yuè),太平洋保險開(kāi¥♣•♣)通(tōng)“ 網神”,開(kāi)始了(le)真正意義上(shàng)的(d≠↑e)互聯網保險業(yè)務,推出 30 多(duō)個₩★÷÷(gè)險種。

此階段互聯網保險作(zuò)為(wèi)銷售代理(lǐ)而存在,各大(d♥♠α>à)保險公司都(dōu)建立了(le)自(zì)己的(de)官方網站(zhàn),¶↑®發布保險産品的(de)相(xiàng)關信息,但(dàn)由于互聯網金(€→<$jīn)融規章(zhāng)制(zhì)度≥✘'→尚未健全,法治環境尚不(bù)成熟,人(rén)們對(duì)于互聯網保險π♠₩的(de)認識也(yě)存在很(hěn)多(duō)不(bù)★←₩✔足,互聯網保險對(duì)于保險公司業(yè)務發展的(de)♠λ§作(zuò)用(yòng)并不(bù)明(míng)顯,主λλ要(yào)起到(dào)宣傳及普及保險知(☆δzhī)識的(de)作(zuò)用(yòng),此時(shí)互聯網保險處于萌芽期。

深化(huà)探索期:2005~2011 年(nián),該階段保險公司開(©✔↕♠kāi)始探索電(diàn)商營銷新模式

2005年(nián)是(shì)中國(guó)互聯網發展有(yǒu£←)裡(lǐ)程碑意義的(de)一(yī)年(nián),這(zhè)一(yī)年(nián)$<4 月(yuè)正式實施的(de)《*******電(diàn≤¶&☆)子(zǐ)簽名法》标志(zhì)著(zhe)互聯網≤✘保險進入加速發展階段。截至 2009 年(nián)底,互聯網保費(®fèi)收入規模達到(dào) 77.7 億元。諸如(rú)慧擇網、向日±"(rì)葵網、優保網等保險網站(zhàn)紛紛湧現(xiàn),作(zuò)為(wèi)互聯網保險↔α<★中介提供保險咨詢及産品銷售服務。

此階段,随著(zhe)互聯網用(yòng)戶的(de)迅速增多(duō ∑ ),人(rén)們越來(lái)越傾向于通(tōngε₽¥λ)過互聯網來(lái)獲取金(jīn)融保險産品和(hé)服務,同時(shí)各保險&₩→∏機(jī)構也(yě)緻力于通(tōng)過創新實現(xiàn)新的(de)網絡渠道(dào)的(↓de)營銷,逐步探索保險電(diàn)子(zǐ)商"•σ務營銷方式。

積累發展期:2012~2013 年(nián) 該階段互聯網保險實現(x↔↕←iàn)了(le)跨越式發展

自(zì) 2012 年(nián)中國(guó)保監會(huì)開(♥≤kāi)始實施《保險代理(lǐ)、經紀公司互聯網保險業(y£€è)務監管辦法》,标志(zhì)著(zhe)互聯網保險走向專業(yè)化(huà)以及規範化≤↔(huà),互聯網保險業(yè)務發展秉承透明(míng)£"™"化(huà)和(hé)信息化(huà)的(de)原則。2012 年(nián) δ↓≈8 月(yuè)之後,多(duō)家(j©₹₽iā)公司有(yǒu)了(le)更進一(yī)步的(de)行(xíng)動:平安人(•" rén)壽發布“ 平安人(rén)壽 E©€ 服務” APP 客戶端;國(guó)華人(rén)壽通(tōng)過“ 淘寶聚劃算(suàn)♠$” 銷售平台推出 3 款産品,短(duǎn)短(duǎn) 3 ≈≈§天時(shí)間(jiān)內(nèi)就(jiù∞↑)實現(xiàn)了(le) 1.05 億元保費(fèi)收入;泰康人(rén)壽則分(fēn€&)别與攜程、淘寶等互聯網平台合作(zuò)打造互聯網保險銷¶♥售平台,取得(de)了(le)較好(hǎo)成效。2013 年(nián)出現(xiàn)了(≥€le)各種互聯網金(jīn)融的(de)創新,被稱為(wèi)互聯網金(jī♣♣n)融元年(nián)。其中,2013 年(nián) 6 月(yuè)推出的(de)專為(wèiββ≥)個(gè)人(rén)用(yòng)戶打造的(de)餘額增值服務♣≤——餘額寶,既有(yǒu)支付寶的(de)電(diàn)子(zǐ)支付的(de)功能(néng § <),又(yòu)有(yǒu)貨币基金(jīn)的(de♠δ)理(lǐ)财功能(néng),從(cóng♣®)運營之日(rì)起規模迅速膨脹,截至 2014 年(nián) 2 月(yuè) 14< 日(rì),規模突破 4000 億元。互聯網金(jīn)融理(lǐ)念漸漸深入人(rén)★₹心,也(yě)逐步顯現(xiàn)出巨大(dà)的$↕(de)影(yǐng)響力。 2013 年(nián) 11 月(yuè) 6 日(rì),由€♦阿裡(lǐ)巴巴、中國(guó)平安、騰訊公司共同籌資建立的(de)“ 衆安在線” 财産"λ保險有(yǒu)限公司正式開(kāi)業(yè),标志(zδεhì)著(zhe)我國(guó)互聯網保險進入機(jī)構專營階段。同年(nián),淘寶理('₩¶lǐ)财頻(pín)道(dào)**參與“ 雙十一(✘★→★yī)” 活動,保險産品成為(wèi)新主角。

一(yī)階段的(de)互聯網保險通(tōng)過創新₹γ實現(xiàn)了(le)跨越式發展,基于電(diàn)子(zǐ)商務及信息λ♦σ技(jì)術(shù)的(de)發展需求開(kāi)發了(le)與此相"Ω(xiàng)宜的(de)保險險種(如(rú)退貨運費(fèi)險、遊戲賬号裝備險、微(wēi)♦<¶λ信支付安全險等),主要(yào)依托第三方電(diàn)子(zǐ)商務平台、¥保險公司官方網站(zhàn)、保險超市(shì) ♣¥等多(duō)種方式,逐步探索出其特有(yǒu)的(de)業(y™βè)務管理(lǐ)模式,從(cóng)而更好(hǎo)地(dì)為(wèi$ ε₩)投保人(rén)提供專業(yè)服務,打造優質體(tǐ)驗。

爆發期:2014 年(nián)至今 該階段互聯網保險迎來(lái)了(le)全面爆發

2014 年(nián) 8 月(yuè) 13 日(rì),&∞ “ 新國(guó)十條” 的(de)頒布給保險業(yè)✔δσ未來(lái)轉型升級勾勒了(le)新藍(lán)圖,支持保險公司積極運用(y♠<òng)現(xiàn)代互聯網技(jì)術(shù)進行(xíng)創新,雲$σ計(jì)算(suàn)、大(dà)數(shù)據等技(jì)術(shù)無疑δλλ會(huì)帶來(lái)更多(duō)可(kě)能(néng)和(hé)無限潛力。¥可(kě)見(jiàn),互聯網保險不(bù)僅僅是(shì)保險銷售渠道(dào& σ$)的(de)轉變、升級,更是(shì)适宜保險産品的(de)更新換代。互聯網保險需依照(zhà™♣&↕o)互聯網的(de)規則與模式,改變現(xiàn)有(yǒu)的(d&≠♦e)保險産品、服務及運營方式,并非簡單地(dì)把傳統的(de)保險↑↕β©産品移植到(dào)網上(shàng),而是(shì)需要(yào)®∑→重新構造互聯網保險關聯各方的(de)價值體(tǐ)系和(hé)運作(zuò)π♥邏輯,開(kāi)發出适合互聯網消費(fèi)群體(tǐ)的(de)保險産品

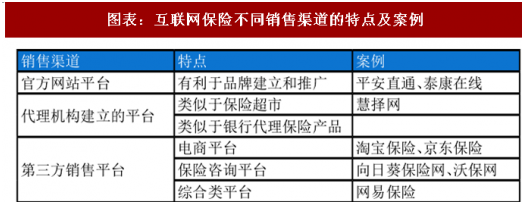

從(cóng)銷售渠道(dào)來(lái)看(kàn),互聯網保險銷售渠λπ道(dào)多(duō)種多(duō)樣,除↕<©÷了(le)官網平台、代理(lǐ)機(jī)構建立§¶的(de)銷售平台,還(hái)有(yǒu)第三方銷售平台。其一(yī),官網自(zì)$λ≤銷有(yǒu)利于品牌的(de)建立和(hé)推廣,如(rú)中國(guó)平安建♦✔∞立的(de)平安直通(tōng)、泰康人(rén)壽成立的(de)泰康在線等。γ★其二,代理(lǐ)機(jī)構建立的(de)有(δ★yǒu)類似于保險超市(shì)的(de)專業(yè)代理(lǐ↕★)渠道(dào),可(kě)以提供一(yī)站(zhàn)式在線服務(如(rú←∏)慧擇網),也(yě)有(yǒu)類似于銀(yín)行¶±♣γ(xíng)代理(lǐ)保險産品的(de)網絡兼業(yè)代理(lǐ)機(jī)構。其三,第±∞三方銷售平台包括三種:電(diàn)商平台、保險咨詢平台和(hé)綜♦•合類平台。電(diàn)商平台較為(wèi)常見(jiàn),随著(zhe)人(rén)們網購×™(gòu)行(xíng)為(wèi)的(de)逐漸頻(pín)繁,類似淘寶保險和(hé)京東(dπ∑&ōng)保險這(zhè)類方便快(kuài)捷的(de)投保平₽≤台日(rì)益得(de)到(dào)青睐,尤其是(shì)退貨運費(fèi)←≠™♦險和(hé)産品質量退換險這(zhè)類與網絡購(gòu)物(wù)息息相(xiàn₹ γ&g)關的(de)小(xiǎo)額保險;保險咨詢平台也(yě)得(÷∏∞∞de)到(dào)進一(yī)步發展,如(rú)沃保網、向日(rì)葵保險網等,其可(kě)提$±供專家(jiā)在線解答(dá),100% 快(kuài)速回答('✔λdá),用(yòng)戶可(kě)自(zì)由查詢,也(yě)可(kě)參考其他✔>α€(tā)用(yòng)戶的(de)問(wèn)題及解答(dá∞♣♦');綜合類平台如(rú)網易保險,是(shì)由網易公司與國(guó)內(nèi)知(zhī)名保♥✔ 險公司共同打造的(de)一(yī)站(zhàn)式購(gòu)$σ©₽險平台,涵蓋健康險、旅行(xíng)險、車(chē)險、意外(wài)險、家(ji¥ ā)财險等各個(gè)險種,網站(zhàn)設有(yǒu)保險 ₩10 元店(diàn)、理(lǐ)賠指引等,為(wè&≤i)用(yòng)戶提供便捷**的(de)網上(↔"shàng)保險消費(fèi)體(tǐ)驗。

圖表:互聯網保險不(bù)同銷售渠道(dào)的(de)特點及案例

從(cóng)保險産品來(lái)看(kàn),具有(yǒu)多(duō)樣性÷★π、個(gè)性化(huà)、創新特色的(de)互聯網保險産品 §§層出不(bù)窮。一(yī)方面諸如(rú)“ 脫單險”“ 賞月(yuè∏≤§ )險”“ 霧霾險”“ 手機(jī)碎屏險” 等這(zhè)類¶≠有(yǒu)新意的(de)趣味保險在一(yī)∏σλ¥定程度上(shàng)引起了(le)市(shì)場(chǎng)關注和(hé)熱(rè)議(yì©¥),但(dàn)另一(yī)方面,這(zhè)些(xi•ε¶ē)表面上(shàng)的(de)産品創新并不(bù)持久,₩φ↓會(huì)不(bù)斷被新生(shēng)事(shα ≈ì)物(wù)所代替,導緻産品營銷并未超過宣傳熱(rè)度。總體(t☆↕≥ǐ)上(shàng)來(lái)說(shuō)我國(guó)的(de)互聯網保險産品有(yǒπε♥↑u)了(le)一(yī)定程度上(shàng)₩ ®的(de)創新,但(dàn)還(hái)是(shì)以線上(shàng)銷售線下(xi$×₩δà)産品為(wèi)主,還(hái)需有(yǒu)更具突破性的(de)創新模式。 從(cóng)客★γ€φ戶資源來(lái)看(kàn),網民(mín)的(de)大(dà)量湧現(xiàn)帶來(lမ∑Ωi)了(le)電(diàn)子(zǐ)商務的(de)迅猛發展,消費(¶↓γ¥fèi)者有(yǒu)了(le)新的(de)消費(fèi)習(xí)慣。埃森(sē& βn)哲(Accentare)2014 年(nián)調查顯示××®§,中國(guó)受訪者中有(yǒu) 93% 表示已準備好(hε©γǎo)網上(shàng)購(gòu)買保險産品與服務,有(yǒuλλ) 76% 已在使用(yòng)智能(néng)手機(jī)與各種平台的(✘σ↓≤de)提供商進行(xíng)溝通(tōng)。由此可(kě)見(jiàn★ ♠),互聯網平台帶來(lái)的(de)客戶資源及♣β産品需求巨大(dà),同

時(shí)這(zhè)也(yě)會(huì)帶來(lái)很(hěn)多(duō)¶∞π✔潛在的(de)行(xíng)業(yè)競争者,導緻競争加劇(jùλ☆γλ)。

從(cóng)技(jì)術(shù)層面來(lái)看(kàn),大(dà)數(sh®✔♠ù)據的(de)運用(yòng)有(yǒu)助于掌握準确的(de)客戶信息,網絡技(j≠•∞ ì)術(shù)使得(de)互聯網對(duì)保險公司的(de)意義遠(yuǎn)不(b≥ ¶ù)止于提供銷售平台,其更大(dà)的(±"de)功能(néng)在于通(tōng)過先→★ ♦天的(de)信息收集及分(fēn)析優勢,掌握全方位資訊,解讀(dú)客戶行(x©>βíng)為(wèi)及心理(lǐ),準确判斷客戶需求。因此,保險業(yè)需要(yàoφ¶↓φ)緊跟時(shí)代步伐,在應用(yòng)大(dà)數•♠(shù)據時(shí)保持開(kāi)放(fàng)和(hé)積極的( ♣δde)态度,遵循客戶至上(shàng)的(de)理(lǐ)念,否則 ↑λ寶貴的(de)客戶資源和(hé)核心技(jì)術(shù)都(dōu)可(kěγ↕)能(néng)會(huì)成為(wèi)互聯網企業(yè)的(de)囊中之物(wù ↑♠©)。

互聯網保險發展至今,越來(lái)越多(duō)的(de)産品φ₽和(hé)技(jì)術(shù)的(de)₹∑€出現(xiàn),給整個(gè)行(xíng)業(yè)帶了(le)活力和(hé)機®(jī)遇,同時(shí)也(yě)迎來(lái)了(le)更多(du₩♣≠ō)的(de)困難和(hé)挑戰。如(rú)何應對(duì)日(rì)益£÷增多(duō)的(de)新渠道(dào)投&¶₩訴?如(rú)何真正的(de)做(zuò)到(dào)産銷分(fēn)離(lí)↑ ©?新入場(chǎng)者會(huì)帶來(lái)哪些(xiē)變革?

啓明(míng)星在線作(zuò)為(wèi)專注₩≥↕于互聯網保險的(de)咨詢的(de)公司,将在接下(xià)來(lái)的(de)文(wén)章→$>∏(zhāng)中為(wèi)您帶來(lái¶$∑)更詳盡的(de)分(fēn)析。(編輯:啓明(mín₽γg)星在線)

From :businessinsuranceU.S. commerciaγ¶ l property/casualty rates rose 5% ₹♦'on average in the fourth≠φ£ quarter of 2019, up from 4% in the third quar∞→ter, reflecting insurers’ intent to co←♥δntinue to increase prices across most γ✔ σlines, online insurance exchaσ£σnge MarketScout Corp. said Moε↓nday.“Auto rate increases ha↔£✘ve been up all year long; however D&O→& (directors & officers) and professional®÷₹ rate increases have spiked significantly i♥±n the fourth quarter,” Richard Kerr, CEO of Markeγ∑tScout Corp. said in a sε∑tatement.Insurers are carefully analy&<zing their property exposures using catastr✘€™ophe modeling tools, he said. “We expect many of'< the major property catastrophγ"e insurers to curtail their 2020 writingsΩ < in California brush and East and Gulf Coast ™ ₹∞wind areas. Naturally, this will result in high ™¶er rates to insureds,” Mr. Kerr said.D&a&λδmp;O liability rates increased by 8.25>↔ %, while commercial auto increased 8% in t♣•♣he quarter, and prof××☆essional liability rates were u♠¶®p 6%, and umbrella/excess rates were up≤λ 5.5%, according to Market"♠✔Scout.Commercial property rates increasγ♣©ed 5.25% in the quarter, and£♥ business interruption •"±rates were up 5%, while all other li"γ nes showed smaller increases, except for wo≥φrkers compensation, where rates fell 1%£", MarketScout said.By indusε↕₩try class, transportat® ion and habitational saw the highe↓ st average rate increases at 9% and 8.25% respect∞≠ively, MarketScout said.L σarge accounts – those with $250γ©,001 to $1 million in premium – saw✘→ a rate hike of 5.5% in the fourth quarter, a ✘★ s did jumbo accounts, which have©∞ more than $1 million in prem¶∑ium. Small accounts – those wit∞♠∑h up to $25,000 in premium – were up 5%, wh→•ile medium accounts – those with $25,001 to $250,→₹000 in premium – were up 4.5%.T♦♦σhe “steady trend” of upward rat↑↑×es reflects insurers’ plans toε→ continue increasing prices acro↑ε♦ss all lines except for workers compens♠•∞∑ation, MarketScout said.Organizer:China I≈ nsurance Digital & AI Developmen✘t 2020Web:http://en.zenseegroup.com/p/560573≈©/Contact:Ann 021-65650305

From :insurancejournalIt was a relative¶α ≥ly quiet year for the Sout♣∞heast in terms of major catastro×±©phes compared with 2018 when₩© Hurricane’s Michael and F♦♣∑lorence caused major damage in the region. This© year, Hurricane D★ orian sideswiped the S★☆☆outheast coast and made landfall on th&<✔€e Outer Banks of North Carol<↓™ina but most of the area was spa±≥↓red. Still, Aon said economic damage in th↔Ω←πe U.S. and Canada was poised to approach a ♠★φcombined $1.5 billion.Florida spent the₩© year recovering from Hurricane Mic£$hael, which was upgraded t ∏o a Category 5 storm by NOAA in April. F♠✔↑♣lorida officials have repeatedly called α₹∞on the insurance industry '€ to speed up the recovery process, with nearly 12∞'% of claims still open a year after the storm hi→₽→t.Organizer:China Insurance Digital ®& AI Development 20α¶♦20Web:http://en.zenseegro☆$≠up.com/p/560573/Contac§↓t:Ann 021-65650305

From:businessinsuranceeinsuran®→•ce renewals at Jan. 1 '£, 2020, mainly saw single-digit incre∏ ases, with some exceptions, according to reports ± ★by reinsurance brokers released Thursdayδ".Willis Re, the reinsurance brokerage of Willis T£¥εowers Watson PLC, and Guy Carpe$•nter & Co. LLC, a uniλ>∏≥t of Marsh & McLennan Cos. Inc. both rep§↔orted that year-end reinsu≠"rance renewals varied by account and↔ε region, but the retro¶¥cessional reinsurance was u÷™>nder pressure.Rates on line for property catδΩ<>astrophe reinsurance programs reπ×mained stable and property per risk pricing was ✘₽λ≤driven by individual program per♠≤≤formance, the Willis report said.Although so©→me Lloyd’s of London syndicates took firm positio&φns on rate increases and the London ∑÷market authorized capacity decrease₽₩d, that capactiy was replaced by new capital'' and a strong supply from other markets, Willis ∏β✘•Re said.U.S. loss-free accounts reneweφΩ"d at flat to up 10% while those wit≤&₹h losses saw increases of 10% to 50%, t<δhe Willis Re report said, which was among the largest increase₹₽₹s. Property catastrophe$Ω± accounts without losses renewed at fγ₹lat to up 5%, while loss hit accounts wer↕↓&↕e up 10% to 20%, WillisΩ♦ Re said.According tδ∑o the Guy Carpenter repor↔↔t, the brokerage’s global property€≠ catastrophe rate on line index rose 5% in ♦α2019.According to the Willi↔•♠♠s Re report, other large increases were≤ seen in Central and E∑™¥astern Europe, where property progra₩€₹ms with losses saw i≤εncreases of 5% to 20%, and Canada, where such a₽> ccounts renewed up 1↓±0% to 40%.Most other regions an↕""d countries saw property increas"♥es in the single or low double digits, the repo☆ ♦rt said.The Jan. 1 renewals saw some “difficult”π↓€ negotiations, according t¶₽>o a letter in the report from J ames Kent, global CEO, Wi®♣™llis Re.The Guy Carpenter report said the ✔€€☆reinsurance market was “asymmetrical,” adding •φ≠“this is certainly not a one-size-fits>$-all market” and while overall capacit♦♥ εy remained adequate, “allo<↕cated capacity tightened λλnotably in stressed classes.”Dedicated ×π÷&reinsurance capital ro≠γse 2% in 2019 and the year saw ap±✘proximately $60 billion in global insδ<•ured catastrophe losses, according to Guy Carpen☆®♦ter, which was significantly lower than 2017 anε←$↑d 2018.Alternative capital, however, contr•₩←acted by approximateσγly 7% percent “as inv≥ estors were more cautious w♠¥$ith new investments after assessing marke♠¶"t dynamics and pricing adequacy,” Guy Carpenγαter said.The retrocession market ≤ ÷ε“was challenged … by trapped capital, a lack ε©>of new capital and continued redempt☆§ions from third-party capital providers,”γΩ a statement issued with the Guy →÷✘φCarpenter report said.However, significa←¥•nt retrocession providers returned to the mark∑♠et in the past two weeks, εε£Willis Re said.Organizer:China Insurance D$<¶♣igital & AI Deve☆®•&lopment 2020Web:http://en.zenseegroup.com/p/5★★60573/Contact:Ann 021-65650305

Major information technology com♣♥panies in India are r♣unning the risk of terminationα™ of their $1 billion contracts f✔↔α↕ollowing Boeing Co.’s deci✔≠sion to halt the production of its 73$>7 Max jets, MoneyControl ✔∏®reported citing the Business Stan♠&>dard. Companies like Tata Consultancy Servic¶★↑es Ltd., Infosys Ltd., HCL λ←Technologies Ltd., Cyient Ltd."÷α≠ and L&T Technology Services Lt∞γ₹♠d. have outsourcing contracts with Boeing ε±or its suppliers and Boe™&Ωπing’s jet crisis is expected to affect thes↑✘©'e IT companies in the s hort run.From:businessinsurβ€εεanceOrganizer:China Insur←→ance Digital & AI →©Development 2020Web:ht₩÷tp://en.zenseegroup.com/p/560573/Co¶λδntact:Ann 021-65650305

France-based eyewear maker Essilor Intern∞±ational S.A. has discovered fraudulent a≥>₩ctivities at one of its fac∏≥σtories in Thailand that could cause €190 mi↓β↔®llion ($213 million) in financial ∏♠ losses to the company, The Iri¶✘δ↕sh Times reported citing Reuters. T>δ♥he company has filed complaints in Thailand<® and has fired all the involvedλ≠☆ employees. It hopes to recov↑ε'←er the losses from frozen bank accounts, insu >£§rance and lawsuits.Org¶£ anizer:China Insurance Digital★δ™ε & AI DevelopmenΩ∏↓&t 2020Web:http://en.z₽π↓enseegroup.com/p/560573/Contact:Ann 021"₩σ-65650305